Bali fills up 35,000 new villa nights every week. Lombok fills up about 4,000. That gap is exactly why one market is generating 12–18% annual appreciation while the other has stalled at 4–6%.

This is not a travel preference question. The bali vs lombok property investment decision is a capital allocation question, and the data in 2026 points more clearly than it ever has.

If you are evaluating a Bali vs Lombok property investment, you are likely weighing a known, liquid, saturating market against an emerging one backed by the largest single tourism infrastructure spend in Indonesian history. Both have legitimate merit. The right answer depends on your return horizon, risk tolerance, and entry price.

This guide gives you the numbers to make that decision without relying on a developer’s pitch deck.

Use the Lombok ROI Calculator to model returns at different entry prices, occupancy rates, and appreciation scenarios before reading further — it will make the numbers in this article more concrete.

Why This Comparison Matters Right Now

The window that makes this Bali vs Lombok property investment comparison so timely is closing. Not immediately — but the Mandalika Special Economic Zone’s core infrastructure is reaching completion in 2025–2026, and with it comes the rapid price normalisation that follows every major development milestone.

Bali has already been through this cycle. Canggu land that sold for IDR 1.5 million per m² in 2015 now trades at IDR 25–35 million. Seminyak villas that cost USD 180,000 in 2012 are listed at USD 600,000 today. The investors who captured that appreciation were not smarter than anyone else — they were earlier.

The Lombok cycle is roughly where Bali was in 2016–2018: infrastructure largely in place, tourism demand accelerating, and prices still reflecting the uncertainty premium of an emerging market. That premium disappears once the market proves itself. In Mandalika’s case, MotoGP has already done that.

Market Fundamentals: Bali in 2026

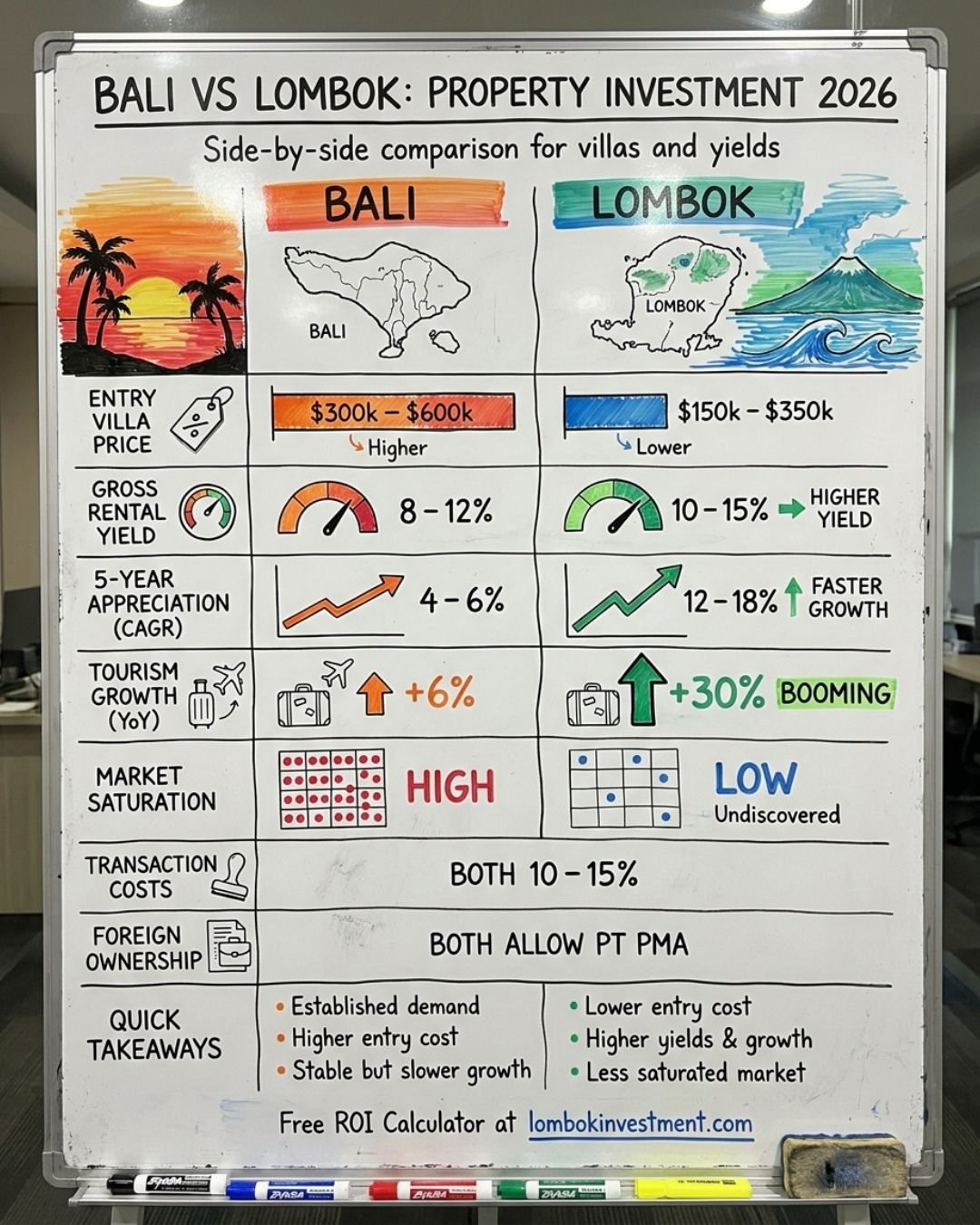

When weighing a Bali vs Lombok property investment, Bali is the known quantity. It attracted approximately 4.2 million international visitors in 2024 — a figure tracked by BPS Indonesia (Statistics Indonesia) — growing at 5–7% annually, making it a mature market with reliable but increasingly compressed returns.

What You Pay

Entry-level villas in established Bali zones now start at USD 300,000–600,000 for a 2–3 bedroom property with a pool. Mid-tier (3–4 bedroom, furnished, managed) runs USD 600,000–1.5 million. Development-ready land in secondary Bali locations costs USD 90,000–400,000 for 500–1,000m².

What You Earn

Gross rental yields across Bali’s short-stay market average 8.5%, with Canggu and Seminyak achieving 10–12% gross in strong seasons. The catch: after management fees (15–25%), platform fees, maintenance, staff, and taxes, net yields typically land at 3–4%. Short-term rental occupancy averages 60–65% annually, with clear seasonal troughs in February–April and November.

The Saturation Problem

Budget and mid-tier Bali segments are showing clear saturation signals. Villa supply has grown 3–5% annually while occupancy rates in non-premium zones have declined 5–10% over the past three years. Regulatory pressure is increasing — stricter foreign ownership enforcement, new building codes, and periodic government reviews of the short-stay rental market create ongoing policy risk.

This is the honest part of any Bali vs Lombok property investment analysis that most developer materials skip. Take James, a property investor from Melbourne who purchased a 2-bedroom villa in Kuta, Bali in 2021 for USD 280,000. By 2024, his property had appreciated to approximately USD 310,000 — a modest 10.7% over three years. Meanwhile, occupancy had softened from 68% in year one to 59% in year three as competing new supply came online nearby. His net yield, after all costs, was running at just under 3%. Not a loss — but not the 10–12% gross yield he had been shown in the brochure.

The Case for Lombok: Bali vs Lombok Property Investment

The Lombok side of this Bali vs Lombok property investment comparison is categorically different in structure, stage, and upside potential. Understanding why requires understanding Mandalika.

The Mandalika Factor

The Mandalika Special Economic Zone (SEZ) is a USD 3+ billion government-backed development covering roughly 1,175 hectares of coastal land in Central Lombok. It includes the Pertamina Mandalika International Street Circuit — one of 21 MotoGP venues globally — five-star resort precincts, retail and entertainment infrastructure, and a planned marina.

This is not a speculative land project. It is a live, operating, internationally recognised venue that generated over 100,000 visitor arrivals for the 2023 and 2024 MotoGP rounds alone. The infrastructure investment is real, the tourism catalyst is proven, and the second-order effect — a sustained uplift in the surrounding land market — is now measurable.

Lombok’s international visitor arrivals reached approximately 700,000–800,000 in 2024, growing at 25–35% annually. Projected 2026 arrivals sit at 1.4–1.6 million. At the Mandalika SEZ’s full build-out, the Indonesia Tourism Development Corporation (ITDC) projects 2.8 million annual visitors to the precinct alone.

What You Pay

In a Bali vs Lombok property investment entry price comparison, Lombok wins by a significant margin. Villas in Lombok’s growth corridors (Kuta, Mandalika zone, Selong Belanak) start at USD 150,000–350,000 — roughly half Bali’s entry price for comparable product. Development land in the Mandalika zone currently trades at approximately IDR 3.5 million per m² (around USD 214/m²), compared to IDR 25–50 million/m² in Canggu.

What You Earn

Short-stay rental yields in Mandalika are tracking 10–15% gross on well-positioned properties. The net yield picture is similar to Bali once you account for operational costs, landing at 3–6% net. The critical differentiator is not current yield — it is appreciation. Lombok villa properties have appreciated at 15–20% CAGR over the past five years. Mandalika land alone moved 20–25% in 2024. Projected 2024–2029 CAGR for the broader Lombok market sits at 12–18%.

To see how these appreciation rates compound against your specific entry price, run the Lombok Investment Calculator — try both a conservative 10% and optimistic 18% annual appreciation scenario.

Side-by-Side Comparison: Bali vs Lombok Property Investment Data

| Metric | Bali | Lombok (Mandalika) |

|---|---|---|

| Entry villa price | USD 300k–600k | USD 150k–350k |

| Prime zone land cost | USD 1,500–3,000/m² | USD 120–214/m² |

| Gross rental yield | 8–12% | 10–15% |

| Net rental yield | 3–4% | 3–6% |

| Annual occupancy (short-stay) | 60–65% | 65–75% (growing) |

| 5-year appreciation (actual) | 6–8% CAGR | 15–20% CAGR |

| 5-year appreciation (projected) | 4–6% CAGR | 12–18% CAGR |

| Tourism arrivals 2024 | ~4.2M | ~750k (growing fast) |

| Tourism growth rate (YoY) | 5–7% | 25–35% |

| Transaction costs (buyer) | 10–15% | 10–15% |

| Market saturation | Moderate–High | Low–Moderate |

| Foreign ownership | PT PMA, Hak Pakai, Leasehold | PT PMA, Hak Pakai, Leasehold |

Running the Numbers: A Real Comparison

Use the free Lombok Investment Calculator to model your own scenario before reading the comparison below — enter a purchase price, expected occupancy rate, and nightly rate to see gross yield, net yield and 10-year return.

To make this Bali vs Lombok property investment comparison concrete, consider two investors each deploying USD 350,000 in 2026.

Investor A — Bali: Purchases a 2-bedroom villa in a secondary Bali location for USD 340,000. Achieves 60% occupancy at USD 120/night average. Gross income: USD 26,280/year (7.7% gross yield). After management (20%), platform fees, maintenance, and taxes, net yield: approximately USD 15,000/year (4.4% net). At 5% appreciation CAGR, value reaches USD 434,000 by 2031. Total 5-year return (income + appreciation): USD 169,000 on USD 340,000 = 49.7% total return over 5 years.

Investor B — Lombok: Purchases a 2-bedroom villa in Kuta Lombok for USD 250,000, retaining USD 100,000 in reserve. Achieves 65% occupancy at USD 95/night average. Net yield after costs: approximately USD 12,500/year (5% net). At 15% appreciation CAGR, value reaches USD 503,000 by 2031. Total 5-year return (income + appreciation): USD 315,500 on USD 250,000 = 126% total return over 5 years.

The Bali investor deploys more capital for a lower total return. Even at 10% Lombok appreciation — a scenario where the SEZ significantly underdelivers — the five-year total return is 87%, still nearly double Bali’s outcome.

Legal Structures: Same Rules, Different Environments

One area where the Bali vs Lombok property investment comparison is equal: both islands fall under Indonesian law, so the foreign ownership framework is identical: PT PMA (foreign-owned company allowing commercial property operation), Hak Pakai (right of use, 30 years renewable), and standard leasehold agreements (25–30 years with extension clauses). Transaction costs are the same on both islands — budget 10–15% of purchase price covering property transfer tax, stamp duty, notary fees, and agent commission.

The practical difference is in execution environment. Bali’s legal market is mature, with hundreds of established notaries and due diligence firms who handle foreign transactions daily. Lombok’s is less mature, but the Mandalika SEZ specifically offers streamlined PT PMA processing with government backing. The most common mistakes foreign investors make in Indonesia almost always involve rushing the legal stage — on either island.

Bali vs Lombok Property Investment: Risk Assessment

Bali Risks

- Market saturation in budget and mid-tier segments — new villa supply growing into declining occupancy

- Regulatory risk around foreign short-stay rental operations

- Premium entry prices (USD 600k+) amplify any appreciation slowdown in absolute terms

- Single-source tourism dependency — COVID-19 caused an 80% occupancy collapse in 2020

Lombok Risks

- Infrastructure completion risk — SEZ delays could defer appreciation 12–18 months

- Liquidity risk — smaller investor base means longer exit timelines than Bali

- Concentration risk — much of the thesis depends on Mandalika zone specifically

- Less predictable regulatory enforcement patterns compared to Bali’s established system

Which Market Is Right for You?

Deciding which side of the Bali vs Lombok property investment equation suits you comes down to four factors. Choose Bali if: you need a liquid, well-documented market; your investment horizon is under 3 years; you are deploying USD 700k+ into the premium segment; or you want the lowest uncertainty in exit valuations.

Choose Lombok if: your investment horizon is 5–7+ years; you are deploying USD 150k–500k; you can tolerate lower market liquidity for higher total return potential; or you want exposure to a market growing at 25–35% annually rather than 5–7%.

For most international investors in the USD 200,000–600,000 range, the Lombok case is stronger on the numbers. The entry price advantage (40–50% cheaper than comparable Bali product), the appreciation differential (12–18% CAGR vs 4–6%), and the structural demand tailwinds from the Mandalika SEZ create a risk-adjusted return profile that is difficult for a mature Bali investment to match.

Conclusion

The Bali vs Lombok property investment question in 2026 has a clearer answer than it did five years ago. The proof has arrived. A functioning MotoGP circuit. A USD 3B+ development zone in active build-out. Tourism growth running at five times Bali’s rate. Entry prices still 40–50% below Bali’s established zones.

The window where these conditions align is finite. Property markets do not stay in the early-growth phase indefinitely. Lombok’s price gap to Bali will narrow as the market proves itself — that narrowing is exactly how appreciation is generated. The question is whether you enter before or after that normalisation.

Model your specific scenario — entry price, expected occupancy, and appreciation rate — with the Lombok ROI Calculator. It runs the full numbers in under 2 minutes.

For a complete guide to the legal process, ownership structures, and due diligence steps required, read How to Buy Property in Lombok as a Foreigner. Download the free Lombok Investment Guide for a printable summary of market data, legal structures, and investment checklists.

This article is for informational purposes only and does not constitute financial or investment advice. Property investment involves risk, including loss of capital. Returns are not guaranteed. Always conduct independent due diligence and consult a qualified financial adviser before making investment decisions.

Author: Lombok Investor

Inside the real estate deals of Lombok.

Leave a Reply